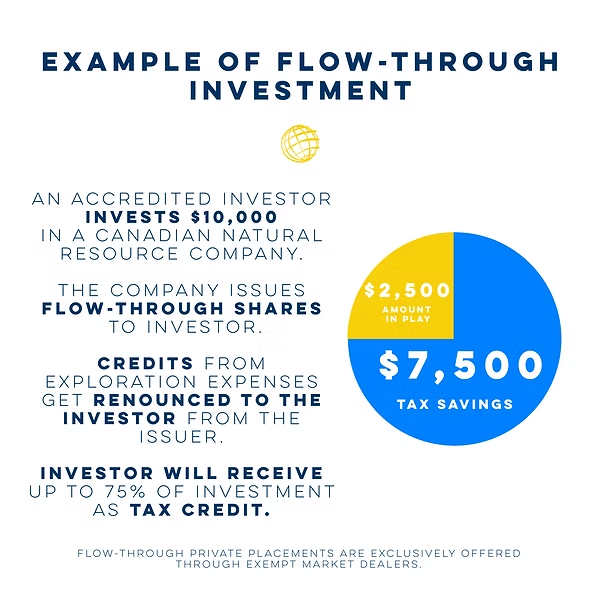

Here’s a visual breakdown of how a typical flow-through share investment works in Canada. The chart shows an investor putting in $10,000, receiving up to $7,500 in tax savings and $2,500 retained in the investment, illustrating how significant the tax benefit can be.

Flow-through shares (often abbreviated as FTS) are a uniquely Canadian investment vehicle primarily used by corporations in the mining, oil and gas, renewable energy, and energy conservation sectors. When a company issues flow-through shares, it agrees to incur qualifying exploration or development expenses and renounce those expenses to investors. The investors can then deduct these expenses as if they have incurred them themselves.

To qualify, the issuing company must be a principal-business corporation (PBC), and there must be a written agreement, commonly referred to as a subscription agreement, between the company and the investor detailing the commitment to incur and renounce eligible expenses.

1. Immediate Income Tax Deduction

Investors enjoy powerful deductions for Canadian Exploration Expenses (CEE), which are 100% deductible in the year renounced, and Canadian Development Expenses (CDE), often deductible on a declining balance basis (around 30%).

2. Investment Tax Credits (ITCs)

Individuals (excluding trusts) may also qualify for a 15% federal ITC on certain flow-through mining CEE amounts. (Government of Canada)

3. Provincial Tax Credits

Some provinces offer additional incentives. For example, Ontario provides a 5% refundable tax credit for investments in eligible flow-through shares linked to mineral exploration.

4. Risk Cushion via Tax Benefits

Because of deep deductions and credits, investors, especially those in high tax brackets, can sustain significant investment losses and still break even. In Ontario, with combined federal and provincial benefits reaching 53.53%, the net cost of a $10,000 investment after tax relief can be as low as $2,159. In other words, investors can lose up to 70–75% of the investment and still not incur a net loss. (Luc Dube)

5. Macro Support from the Federal Government

In March 2025, Canada extended its mineral exploration tax credit for two additional years, ensuring continued access to a 15% tax credit for investments in flow-through shares of smaller mining companies. This measure is expected to inject C$110 million to support exploration activity.

While the capital gains tax increase in 2024 raised concerns, since flow-through shares produce capital gains that might now be taxed at a higher inclusion rate, the outstanding FTS issuance remained strong. In 2023–2024, investors continued supporting junior mining ventures heavily via FTS, which accounted for more than 65% of exploration financing on TSX Venture Exchange.

Ideal for:

Key risks and considerations:

When evaluating flow-through share opportunities, staying abreast of corporate filing details, regulatory updates, and sector shifts can be daunting. This is where Avantis AI comes into play:

By leveraging Avantis, professionals can streamline evaluation of flow-through share issuers, mitigate compliance risk, and uncover their strategic edge in the fast-moving resource exploration space. Flow-through shares continue to be one of Canada’s most potent tax-based incentives for channeling capital into resource exploration. Investors stand to gain greatly via tax deductions, credits, and a naturally built-in downside cushion. With the government's ongoing support through extended tax credits, and despite macro challenges like capital gains reform, FTS remain a vital tool in 2025. That said, due diligence is critical, particularly around issuer eligibility, provincial rules, and documentation. Tools like Avantis AI offer a modern solution, helping investors and advisors navigate filings, regulatory updates, and corporate disclosures efficiently.

Ready to optimize your market research process?

Contact Avantis today for a personalized overview and free trial.

Get Started with Avantis for Free

Get Started with Avantis for Free

88 Queens Quay West, Suite 2500, Toronto, ON, Canada M5J 0B8

(289) 803-8222

© 2025 Avantis AI Inc.